Have you ever noticed how we all tend to wonder “What’s wrong with the world?” This negative slant has become a fixation. Seeing only the worst, our ability to picture what is right is undermined.

The contrarian fellow asks “What’s right with the world?” to get his mind travelling in an altogether different direction. Right thinking requires being fully present and objective. To approach the truth, we must drop our stories and see with untainted eyes.

Here are things that we find are right with the world.

At the G20 summit in November, Joe Biden and Xi Jinping struck a positive note.

The US should “compete vigorously” with China, Biden said, but he was not seeking a new Cold War. Xi admitted that US–China relations were not meeting global expectations and that they need to be set on an “upward trajectory.” The two countries agreed to resume bilateral talks on climate change and create channels for their top officials to communicate regularly.

Biden emphasized that America’s “One China” policy had not changed, despite several divergent comments and Nancy Pelosi’s July visit to Taiwan. In exchange, Xi told Vladimir Putin using nuclear weapons would be “an existential error” and that it was time to resolve the Ukraine conflict. Wang Yi, then China’s Foreign Minister, called the three-hour meeting “a new starting point.”

Around the same time, Warren Buffet’s Berkshire Hathaway disclosed a $5 billion stake in Taiwan Semiconductor Manufacturing Company. This is an omen. It suggests to us that Buffet is clearly not concerned about China seizing Taiwan, unlike everyone else we know. Political tensions seem to be easing when it comes to US–China ties and the cross-strait relationship.

Source: Associated Press

In December, Beijing hosted the annual Central Economic Work Conference (CEWC), the most important Communist Party-led annual economic meeting. After acknowledging that 2022 had been a “turbulent year,” China’s top leadership has set its sights on boosting economic growth. There was noticeably less discussion of common prosperity or of “reining in capital.”

The most economically crippling measures—quarantines, community lockdowns, and travel restrictions—have all been completely abandoned. And Beijing has put an end to property-sector deleveraging, launching a series of policy initiatives to restore demand for new housing and to boost construction. The CEWC signaled an active fiscal policy for the year ahead.

Officials have also been shifting toward a more constructive stance when it comes to tech platforms. Tencent secured a green-light for releasing new games, and Chinese regulators approved a plan by Ant Group to raise $1.5 billion for its consumer-finance unit. More positive news is coming out of China now than has been the case for the past year or two.

After Russia invaded Ukraine ten months ago, it appeared that the world would be in danger of running out of oil and gas supplies. Oil prices are back to pre-war levels, however, and prices at the pump are falling. The national average for regular gas has dropped to $3.20 after reaching a record $5.00 per gallon on June 14. A $1.80 decrease in gas prices equals to about $225 billion a year in savings for US households. That’s equivalent to nearly 1 percent of GDP.

European natural gas prices have fallen well below their pre-war levels, reflecting both the continent’s success in securing alternatives to Russian gas and widespread conservation efforts. A relatively mild winter also helped. Russia used to provide about 40 percent of Europe’s natural gas. “We now have a well-supplied EU gas market, even without Russian gas,” said Henning Gloystein, director at Eurasia Group.

Despite all the doom and gloom, economic expansion in the eurozone has persisted and its GDP has recovered 6 percent since 2021, on par with the US. There is no labor shortage, and the labor participation rate has largely returned to pre-pandemic norms. Wage growth is still subdued. European stocks are outperforming the US in dollar terms from the 2022 lows.

Source: Foreign Policy

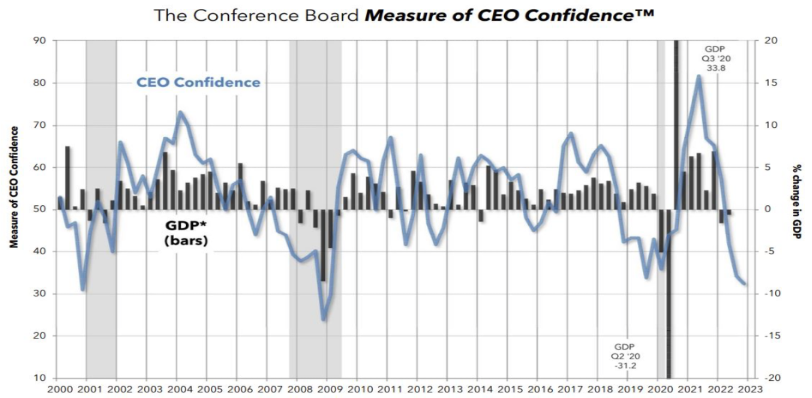

Survey results show a decline in CEO confidence, which points to a softer outlook for hiring and business investment. Such feelings haven’t materialized, however, in widespread layoffs or cuts to capex. S&P 500 companies spent $222 billion on capex in the third quarter compared to $176 billion in the same quarter a year earlier.

The 0.9 percent national layoff rate is well below the average of 1.3 percent in 2019, a year that enjoyed the strongest labor market in decades. In 2022, weekly jobless claims averaged 220,000. That figure averaged 369,000 in the 2010s. Job openings have fallen by about 1.5 million but remain higher than at any time before the pandemic.

Executives may be talking about recession risks more, but what they are doing seems to be quite different.

Despite months of downward revisions to expected earnings, the consensus is for S&P 500 earnings to grow 5 percent in 2023 (earnings per share coming in at $231). “We can debate whether or not we are going into a recession but there is no recession in corporate earnings,” said Howard Silverblatt from S&P Dow Jones Indices. “Cash flow is still there.”

In 2022, companies flexed pricing power to support earnings. While the decline in goods inflation is a headwind for pricing and revenues, companies may benefit from declining COGS given supply chain issues have resolved and transportation costs are much lower. A weaker US dollar should also help profits.

Actual earnings reported by S&P 500 companies over the past five years have exceeded estimated earnings by an average of 8.9 percent, according to FactSet. On a ten-year horizon, the positive earnings surprise was 6.5 percent.

Source: The Conference Board

Financial conditions tightened sooner and more sharply than anyone expected. Yet there are no indications that the US economy or financial system are under any stress. It didn’t “break” anything apart from the speculative froth in the stock market. Consider the following:

(1) The credit spread between the high-yield corporate bond composite and the 10-year US Treasury has widened from 279 basis points at the start of 2022 to 462 basis points (down from 600 basis points in July). It isn’t spiking higher as it did during previous credit crunches. In 2011, it reached 1000 basis points; in 2008, 2000 basis points; and in 2011, 2016, and 2020, it reached 800 basis points.

(2) Bank loans in the US were up more than $1 trillion in 2022 to a record high of nearly $12 trillion. Loan balances grew across all major loan categories, with commercial and industrial (C&I) and consumer loans growing above 10 percent. The aggregate loan delinquency rate is at 17-year lows and loan loss provisions remain below their pre-pandemic level.

There is growing debate within the FOMC as to how far the Fed should go, a welcome shift from the uniform hawkishness a few months ago. Soft inflation data raises the odds that the Fed will conclude its rate-raising campaign at the next meeting or soon thereafter.

Core inflation has risen at a 4.2 percent annual rate over the last three months. That’s well below the recent peak of 7.9 percent registered in the spring. Indeed, core prices rose only 0.2 percent in November, the lowest since August 2021. That works out to a 2.4 percent annual rate, which is consistent with the Fed’s inflation target.

Shelter costs slowed in November and private-sector readings show rent prices are falling, which will feed through to the official inflation reading in the coming months. Price gains across other services, excluding shelter, are flat. The strong labor market isn’t influencing prices to accelerate.

Treasury breakevens—the rate of future inflation suggested by the difference between yields on regular and inflation-protected bonds—suggest inflation will average roughly 2.2 percent over the next five years, well below last year’s peak expectation of 3.6 percent.

Source: Reuters

Since mid-June, the Fed has hiked 350 basis points and the market is pricing another 50-basis-point hike. The Fed’s balance sheet has shrunk by $404 billion to $8.5 trillion, 5.5 percent below its April peak. And yet the return of the 7–10-year Treasury index is just minus 1 percent during this time. The 10-year yield is at 3.5 percent today versus 3.4 percent in mid-June; the S&P 500 is up 6 percent, and the dollar is flat.

How could this be the case? What is the market telling us?

When prices are moving contrary to general expectations, our minds get stuck or mired in worry. If we have already convinced ourselves of a bear market, we are unlikely to change our outlook until the new bullish trend becomes too obvious to ignore. With eyes wide shut, most people don’t expect to see what they’re not looking for. We encourage you to open your eyes.

A year from now we’ll wonder: What’s wrong with people? Why wasn’t anyone buying when prices were low?